Every investor has their own 💰financial goals and 📈success metrics. Here are mine.

Finding your north star metric as an investor can be confusing. Do you care more about consistent cash flows overtime or a large lump-sum payment later in the future? Do you care about total cash returned or a risk-adjusted rate of return? Even the most experienced investors have trouble keeping track!

Whether you’re a casual weekend investor or experienced limited partner, there are dozens of metrics to track success. My hope with this article is to explain a few important metrics in plain and simple English (complexity is always a deal killer). Choose the ones that best fit your strategy and let me know on Twitter if I missed any or can improve my explanations.

TLDR! (too long; didn’t read)

After spending weeks writing this post, I sent it to my buddy Roy Schillock (CFA, private wealth manager, and MBA candidate 2022) for review & edits. To my excitement (and chagrin lol), he took my 2000+ word article and essentially “nailed it” in two simple paragraphs and one small chart:

After serving billionaires and centimillionaires (most of whom don’t really get this stuff anyway), I’ve learned everyone defaults to thinking in %s or $s. Plain and simple: use Internal Rate of Return (IRR) and Total Value per Paid-in-Capital (TVPI) together. They’re a bit meaningless alone, but together, they tell the story pretty darn well.

This chart shakes out all the noise pretty effectively. IRR tells you how something does in % terms, accounting for the time value of money, but not in dollars. TVPI tells you how something does in $s but excludes % and time value of money. Together you got a feel for all three. Even though we can rarely articulate it cleanly, people need a decent performance in both terms. Use IRR and TVPI to triangulate where performance actually is.

Not sure what IRR or TVPI is or why they’re important? Below I explore both topics as well as my non-exhaustive list of common metrics that I track across my portfolio.

NOTE: Almost every metric listed should have “net” proceeding it. The difference between gross vs. net represents whether we account for the firm’s fees & costs in our math. I don’t use net in this post for the sake of brevity, but you should when running your calculations.

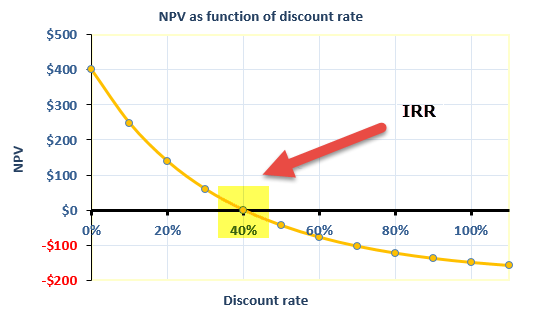

IRR: Internal rate of return

Let’s start with probably the most well-known metric and my personal favorite: IRR. I consider IRR the metric of all metrics. In my experience, it’s one of the most important metrics used in determining the success of an investment. It’s an a posteriori metric since it’s really only useful after the investment is completed. The most technical definition of IRR is the “rate of growth that equilibrates incoming and outgoing cash flows.”

Said another way, it’s the “rate of return that sets the net present value of all cash flows (both positive and negative) from the investment equal to zero.” I found this youtube video to be helpful.

Breaking this down even further, IRR helps me answer the question, “Which of my investments is performing the best over time regardless of risk or asset class?” It lets me look back at two very different investments and figure out which provided better returns.

If there is one thing you remember about IRR, it’s this: IRR factors in the time value of money. For example, an investment that doubles your capital within a few years will have a much higher IRR than one that doubles it ten years from now.

Why is it important?

Because IRR takes into account the time value of money, it can be used to compare the success of multiple investment opportunities. If you have limited capital to deploy and multiple investments to choose from, ceteris paribus, choose the one with a higher IRR. Or, if you want to see which of your fund managers are performing better, after many years of investing with them, you would run an IRR analysis on each of their investments or funds.

Caveats

Couple of things to mention about IRR. Firstly, the IRR doesn’t account for risk. One investment may have produced a phenomenal IRR, but it could have been extremely risky. Personally, if the projected IRR between two assets is relatively equal, but the risk to achieve that return is vastly different, I will choose the lower IRR since the risk is much lower (i.e., real estate investment vs. tech startup investment).

Secondly, IRR is best calculated after the investment is completed. Projected IRR is merely a guess by the fund or firm manager(s). Even when you’re midway through an investment, IRR can be misleading. There are better metrics (written below) that are worth using instead.

Lastly, my friend Dorian recently brought it to my attention that some more prominent investors care less about IRR and more about their cash multiple. More on this below.

How to calculate it

Use excel (xirr function), or google it — it’s a very common formula.

Cash multiple: Cash-on-cash return

The cash-on-cash return is a quick calculation to determine how much money you are receiving each year from an investment. There is NO time factor with this metric — the yield is averaged over the entire tenure of the investment. The simplicity of this calculation is both its greatest strength and weakness (see below). Expressed as a multiple, it’s the money received from an investment compared to the total investment amount; the formula is:

Cash-on-cash multiple = annual cash flow : total cash invested

As a straightforward example, if you invest $100,000 into investment A and the same in investment B, and A pays you back $200,000 next year while B pays you the same, but in 10 years, then both investments would have a 2x multiple.

Do you see how this metric does not have the time value of money? Both returned 2x, yet B took nine additional years!

Personally, I don’t use this metric beyond simple napkin math because of this shortcoming, but my friends in finance tell me it becomes more popular the richer you get. If you think about it, that kind of makes sense — good luck getting high IRR when you have billions to invest. At some point, you simply ask how much can you make me if I give you X millions, regardless of time. I can imagine a world where I have an ungodly amount of money and simply live off the interest.

DPI: Distributions to paid-in-capital

Because metrics like IRR are insufficient to help limited partners calculate an investment’s success during its life (vs. at the end), there are other metrics we can use instead. One of those metrics is called DPI, or distributions to paid-in-capital.

Distributions: the total amount of money an investor has received from the fund.

Paid-in-capital, sometimes called “contributed capital” or “called capital”, is the total amount of money an investor has paid into the investment or fund. Note this is different from “committed capital”, which is the amount an investor has promised to contribute. For example, if you agreed to invest $1 million, many times the money isn’t collected upfront but instead over the lifetime of the fund.

The distinction between paid capital and committed capital is important because it eventually affects the IRR calculation. Remember IRR takes into account the time value of money? Well, if the fund collects all the money upfront but takes many years to deploy it, that will hurt the investment’s IRR. Thus, fund managers are smart — they only ask for the money when they need it.

The DPI formula is distributions / paid-in-capital

DPI is a ratio that is expressed similar to multiples: 1x, 2x, 2.5x, etc. The higher the number, the better.

By way of example, let’s say an LP has committed $1 million each to two different funds. Fund A has collected $100,000, and Fund B has collected $50,000. Furthermore, Fund A has paid out $75,000, and Fund B has paid out $20,000.

So far, which fund is performing better? Well, great opportunity for DPI!

DPI for Fund A: $75,000 / $100,000 = 0.75x

DPI for Fund B: $20,000 / $50,000 = 0.4x

It looks like Fund A is performing better! Even though it has collected more money from the investor, it has returned much more capital.

RVPI: Residual value to paid-in-capital (Unrealized Multiple)

I like to joke that RVPI is DPI’s younger sibling that hasn’t grown up yet. To understand why let’s first define “residual value.”

Residual value is the total amount of remaining money and assets in the fund or investment if it was fully liquidated today. After liquidating the assets and paying off any liabilities, the amount left is the residual value or unrealized returns. A reader, Carlos Torres de la Cuba, pointed out this is called an ASC 820 valuation — it turns out calculating a private, illiquid asset is more complex than you think!

RVPI is more popular in the early years of an investment before any distributions have been made. The joke about the younger sibling should now be obvious: the residual value represents assets and growth that has not yet been realized.

Although important, this metric is a bit theoretical because a) we assume the recorded fair market value of the assets is accurate, and b) the fund’s assets are liquid enough for us to sell them all immediately without taking a hit on their value.

The RVPI formula is residual value / paid-in-capital. Like the previous metric, RVPI is also expressed as a multiple: 1x, 2.5x, 4x, etc.

Note that the LP’s contribution is part of the residual value, it’s not considered a liability.

I generally don’t use this metric but see how it can be helpful, especially if you are trying to ascertain a fund manager’s success or investment opportunity. If I had a lot more money at stake and needed to keep close track of it, I’d probably lean on this metric a bit more.

TVPI: Total value to paid-in-capital

Another metric I don’t use too often but still worth mentioning is TVPI, total value to paid-in-capital. Although I don’t bother calculating this metric myself, I do find it nice when fund managers report it, and it’s something I would scrutinize a bit more as the manager begins to raise their next fund.

Total value is the sum of all the distributions made to investors and any residual value.

The TVPI formula is (distributions + residual value) / paid-in-capital

This metric is important if an investor wants to know their total return from an investment or fund. The metric accounts for all the money the investor has received to date and all additional money they will receive (residual value) after selling off all the funds assets.

A related investment concept to TVPI is called the investment “J-Curve”, as represented in the graphic above. This curve represents the TVPI over time. Notice how in the beginning, our return is less than 1x, which means we are underwater (a lousy investment). But over time, hopefully, our return grows and so does the TVPI! This famous investment graph is called a J-Curve because its shape looks like a J. Professional investors don’t expect immediate returns and are usually okay with the curve part of the J since the investment is still in its infancy.

PB: Payback period

This metric is straightforward and easy to remember. The payback period is the number of years it takes to receive back your original investment. For example, if the initial investment is $10,000 and the annual payouts are $1,000, then the payback period is ten years.

I actively track this metric and like this metric, because it helps me know when I’ve been paid back fully, and the rest is profit. It helps me sleep just a little bit better knowing that I received my original investment back.

Limited partner investment metrics

If you are also actively investing across multiple asset classes with a long-term investment horizon, I’m curious how you measure success? Please let me know in the comments below!

Very straightforward Very helpful. Easy to understand. Thanks Ben.

It would be nice if there was a metric such as WTIBAG “Will this investment be any good” These are great metrics but they must be applied against the brains and integrity of the sponsor (GP) of the investment. Great metrics combined with a bad sponsor= No return on investment

The TL;DR section in the beginning was a great summary before diving into the articles.

I like to also look at the strength of the underlying companies, including their cash runway, quality of revenue, etc. Another factor I consider is whether weakness exists in the manager’s historical portfolio construction, and whether the stage the dollars invested reflected the true thesis the manager set out to do. They should adjust and adopt any learnings from a prior fund, and be able to support them with why.